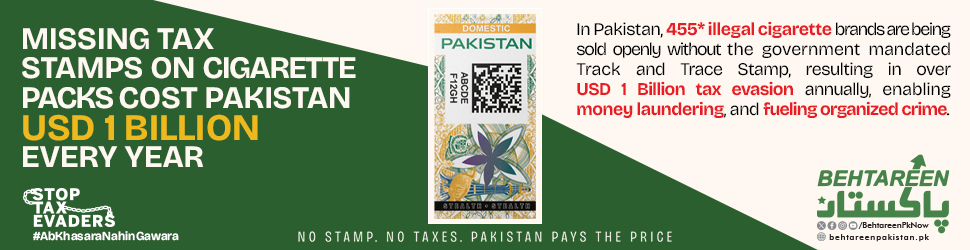

A woman in Rawalpindi receives a call from someone claiming to be her bank. He knows her account number. He knows her last transaction. He asks for a one-time password to “secure” her account. Within minutes, her savings are gone. Her SIM was cloned. Her bank account was already mapped. The fraud took eleven minutes. Her complaint journey took eleven months and went nowhere.

This is not an edge case. This is Pakistan’s digital economy in 2026.

Last quarter alone, Pakistan processed 3.4 billion retail transactions worth PKR 167 trillion, with 92 percent flowing through digital channels. Forty-eight million citizens are registered on Raast. JazzCash serves 58 million customers. Easypaisa became a licensed digital bank in January 2025. By every metric of reach and scale, Pakistan’s digital transformation is a success story. Yet FIA recorded over 73,000 cybercrime complaints in 2024 nearly 36,000 of them financial fraud. Banking Mohtasib complaints rose 15 percent in 2025. The woman in Rawalpindi is not an outlier. She is a data point in a pattern that Pakistan’s institutions are not yet measuring together.

The first public sector-by-sector digital trust benchmark of Pakistan — the Pakistan Digital Trust Index 2026 — scores telecom at 68 out of 100 and digital banks at 67. Both sit in a transitional zone: strong enough to digitise, not yet strong enough to digitise safely. That distinction matters enormously because transitional trust at scale is not a minor gap. It is a structural leak in a system processing hundreds of trillions of rupees every year.

The source of that leak is not incompetence. Pakistan’s institutions are individually impressive. NADRA has conducted over 640 million biometric verifications and upgraded national identity credentials with QR-based verification in February 2026. PTA’s DIRBS has blocked 72 million fake device IMEIs. SBP has consolidated customer onboarding standards and extended conduct regulations to digital banks and electronic money institutions. These are real achievements. The failure is that none of these systems speak to each other in real time, with shared fraud data, shared taxonomy, or shared escalation protocols.

In March 2026, a single raid in Pattoki exposed exactly how that silence is exploited. Investigators found illegal SIM activations, biometric device tampering, 224,201 stored digital fingerprints — and direct links to microfinance bank accounts. One criminal operation. Three regulatory domains. Zero shared early-warning system. That raid should have been prevented six months earlier by cross-sector intelligence. It was not, because the architecture for sharing that intelligence does not yet exist.

Four things need to happen — and none of them require new legislation.

SBP must publish a quarterly public fraud dashboard covering fake-call fraud, QR fraud, account takeover, and mule-account closures with institution-level recovery rates. The data already exists inside banks. Making it visible changes incentives overnight.

PTA and SBP must formally designate illegal SIM issuance as a shared financial risk. The Pattoki evidence is unambiguous. The regulatory response must match it.

NADRA’s Nishan Pakistan and QR-based identity verification must be operationalised as reusable cross-sector trust services — one verified identity usable across banking, telecom, and government portals. Pakistan’s identity rail is its strongest asset. It remains stubbornly underdeployed.

Finally, the federal government must establish a Digital Trust Council — SBP, PTA, NADRA, FIA, NCCIA, SECP, and industry at one table, with published outcomes and allocated responsibilities. Singapore did exactly this and recovered S$140 million in scam losses in 2025 alone. Pakistan has every institution Singapore used. It is missing only the table.

For the CEOs and presidents of Pakistan’s digital banks and telecom operators, this is no longer a compliance question to delegate downward. Your fraud exposure is now publicly measurable. The question is whether you have the internal architecture to manage it — or whether a regulator, a journalist, or a Banking Mohtasib report will manage it for you.

Pakistan did not build 197 million mobile subscribers and a real-time payments network to lose public trust one fake call at a time. The infrastructure exists. The will to connect it is what is missing. That window will not stay open once 5G scales the risk further.

The woman in Rawalpindi is still waiting for her money back. She should not have to wait for a council meeting to be convened before someone takes responsibility.

The author recently published the Pakistan Digital Trust Report 2026, the first public benchmark of digital trust across Pakistan’s telecom, banking, fintech, government, and e-commerce sectors. https://www.linkedin.com/in/faisal-aziz-gill-9a45211b5/

Comments are closed, but trackbacks and pingbacks are open.